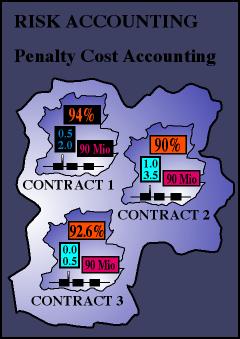

The three contracts

show the following specifications:

Contract 1:**** Sales

Price: 90 Mio $****Guarantee:

94 %****Penalty

/1% / Refaund /1%: 2 Mio $ / 0.5 Mio $

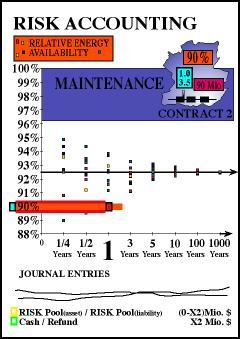

Contract 2:**** Sales

Price: 90 Mio $****Guarantee: 90 %****Penalty

/1% / Refaund /1%: 3.5 Mio $ / 1 Mio $

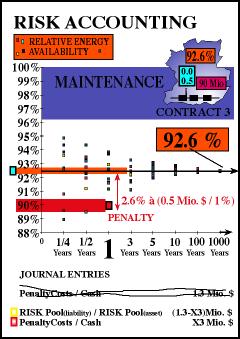

Contract 1:**** Sales

Price: 90 Mio $****Guarantee: 92.6 %****Penalty

/1% / Refaund /1%: 0.5 Mio $ / -

According to contract

1, the buyer and the seller have agreed

upon a guaranteed level of energy availability

at the end of the year of 94%. Furthermore,

a penalty of 2 Mio $ per 1% of lower energy

availability will be charged and must be

paid by the seller. In the case of producing

more than 94% energy availability, a refund

of 0.5 Mio $ will be transferred back from

the buyer to the seller.

The other two contracts

can be interpreted in analogy. Contract

3 is insofar special as there are no refunds

paid at all and both the expectation of

the energy availability and the guaranteed

corresponding figure is the same.

In this example,

the sales price will not be investigated

because it does not influence the yearly

cash flow volatility with respect to our

underlying RAM distribution.

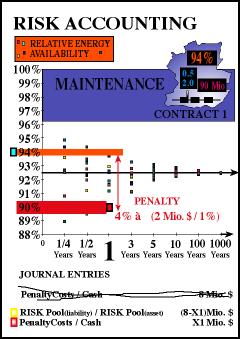

We assume that at

the end of the year all three plants produce

the same amount of energy. Let us further

assume that the observed energy availability

is by random 90%. Remember, that the three

plants are exactly the same as far as their

structure and their failure-, and repair

rates are concerned, thus the underlying

drivers in form of our RAM distribution

curve is exactly the same, too. The only

difference is that the applied financial

contracts between the buyer and the seller

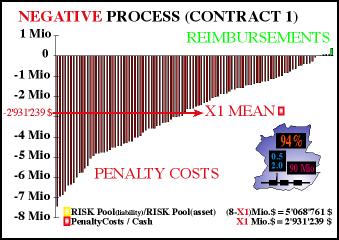

have other specifications. According to

contract 1 a penalty of 4% à 2 Mio

$ = 8 Mio $ has to be paid at the end of

the year. Do we have to punish the seller

of contract 1?

The NOT risk adjusted

journal entry would be: Penalty Costs /

Cash 8 Mio $.

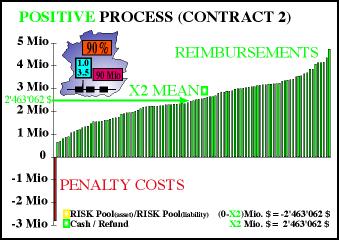

By random, the guaranteed

(set in advance) and the observed (at the

end of the year) energy availability of

the plant 2 (contract 2) are alike. No cash

will flow out of the organization. What

about the salesman of contract 2? Is he

really in a neutral position? In such situations,

a not risk adjusted accounting would not

apply any journal entries. Within a fully

risk adjusted accounting system, we do have

to generate 2 journal entries, one of them

is profit & loss effective, the other

is not. |